CPA Construction Industry Scenarios 2020/21

Construction Products Association says industry bouncing back despite W-shaped recession and recovery

THE Construction Products Association’s latest ‘Construction Industry Scenarios’ sees a W-shaped economic recession and recovery as its main assumption, with construction output expected to rise 14% in 2021 and 4.9% in 2022. This takes into account the new lockdown restrictions over winter 2020/21 before a sustained recovery from the second quarter of this year as vaccines are rolled out and the services-based economy starts to reopen again.

The CPA says that while some sectors of construction are dependent on consumer and business confidence returning, construction activity has largely been able to bounce back quicker than the overall economy. With government making it clear that the construction and manufacturing sectors should continue to operate despite COVID-19 restrictions, output has been able to rise and recover relatively rapidly.

The 14.0% rise in 2021 follows an estimated contraction of 14.3% overall in 2020 caused by the sharp fall in the first half of last year. It should be noted, however, that output is only expected to recover to pre-Covid levels in 2022. There is also the risk that once the furlough and self-employment support schemes end in April, there may be a sharp rise in unemployment that could potentially dampen this recovery.

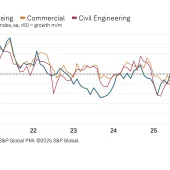

The CPA’s Scenarios show that private housing was one of the quickest sectors to recover in 2020, with mortgage lending and property transactions above pre-Covid levels at the end of the year. Pent-up demand as well as the Government’s stamp duty holiday and the end of the first phase of Help to Buy largely drove the recovery in this sector. Demand for private housing is expected to moderate in 2021 after these policies end on 31 March and then subsequently pick up once again in line with the economic recovery throughout late 2021 and 2022.

A slower recovery has been seen in the commercial sector, with store closures and low rent collection in retail and leisure as well as the shift to working from home causing uncertainty for the offices sub-sector. Recovery in 2021 and 2022 is further constrained by the long-term shift to e-commerce in retail, which is likely to have been accelerated by consumers switching to online purchasing during the pandemic. The ongoing question of whether the shift to homeworking will continue after the vaccines are rolled out will be crucial to determining demand for offices space.

Homeworking has, on the other hand, had a positive impact on the private housing repair, maintenance and improvement (RM&I) sector, with households investing accumulated savings from lower daily expenditure back into homes. Although the trajectory for future demand is dependent on labour market conditions as job support schemes end in April, the extension of the Government’s Green Homes Grant may help to boost activity. For public housing, a backlog of cladding work is expected to drive activity in RM&I in 2021 and 2022 as the Building Safety Programme moves beyond the removal of aluminium composite material.

Commenting on the winter Scenarios, the CPA’s economics director, Noble Francis (pictured), said: ‘The spectre of a ‘no deal’ Brexit that would have badly affected the UK economy and construction in the short term has been avoided, but questions over the long-term impact of COVID-19 on the structure of the economy still remain.

‘This continues to leave questions about the fortunes of certain construction sectors. This is most notable in the commercial sector, where there is still lots of uncertainty about the future of retail and office space. It will be crucial to observe how businesses change their operations as the vaccine is rolled out in the coming months and to what extent there is a ‘return to the office’.

‘While the fortunes of some sectors have been tied to Covid restrictions and associated business and consumer confidence in the wider economy, infrastructure has largely escaped such uncertainty. Projects have been able to effectively enact safe operating procedures given the sector’s large construction sites that have fewer different trades mixing than in most sectors.

‘As such, infrastructure has been least affected by Covid restrictions and output is expected to lift the whole industry over 2021 and 2022. Main works on HS2, Europe’s largest construction project, along with offshore wind and nuclear projects are expected to be the main drivers of activity.’