Total UK construction activity rises for third month running

Construction output rises again in April, despite fastest fall in housing activity since May 2020

UK construction companies remained in expansion mode during April, but the latest survey data indicated uneven growth across the sector. Rising volumes of commercial work and civil engineering activity helped to offset the steepest decline in residential construction output since May 2020.

At 51.1 in April, the headline seasonally adjusted S&P Global/CIPS UK Construction Purchasing Managers’ Index (PMI) – which measures month-on-month changes in total industry activity – was up slightly from 50.7 in March and above the neutral 50.0 value for the third month in a row. However, the latest reading signalled only a marginal overall expansion of construction activity.

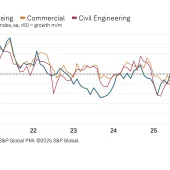

Commercial building was the fastest-growing area of the construction sector in April (index at 53.9), with improving economic conditions helping to boost clients' willingness to spend. The rate of expansion was the second strongest since October 2022, although survey respondents again cited a growth headwind from squeezed client budgets and elevated cost inflation.

Civil engineering activity (index at 52.0) also picked up in April, supported by resilient pipelines of work on infrastructure projects, whilst house building was by far the weakest-performing segment in April (index at 43.0). The rate of decline for total residential work was the steepest for nearly three years. Survey respondents commented on delays to new house-building projects, alongside constraints on demand from softer market conditions and higher borrowing costs.

Construction companies anticipate a further increase in business activity during the year ahead, but the degree of confidence edged down to a three-month low. Around 44% of the survey panel forecast a rise in output in the next 12 months, while only 13% expect a fall. Survey respondents mostly commented on optimism due to resilient client demand. Some firms, nonetheless, noted concerns about subdued housing market activity, rising interest rates, and the uncertain economic outlook.

Tim Moore, economics director at S&P Global Market Intelligence, who compile the survey, said: ‘The construction sector stretched out its current phase of expansion to three months in April, signalling a modest rebound from the downturn seen at the turn of the year.

‘Commercial building work continued to outperform, helped by stabilizing domestic economic conditions and a gradual rebound in business confidence. Civil engineering activity was also a driver of construction growth during April, with rising infrastructure work contributing to the best phase of expansion in this segment since the first half of 2022.

‘However, the return to growth for UK construction output appears worryingly lopsided as residential work decreased for the fifth successive month. Extended delays on new housing starts were reported again in April, due to a considerable headwind from elevated mortgage rates and weak demand. While there have been some signs of a recent stabilization in market conditions, this has yet to feed through to construction activity. In fact, the latest reduction in residential building was the fastest since May 2020.

‘On a more positive note, the latest survey illustrated a further slowdown in input price inflation across the construction sector,’ added Mr Moore. ‘Softer cost pressures partly reflected a sustained improvement in supply chain performance, with lead-times for deliveries of products and materials shortening to the greatest extent since September 2009.’