May sees modest upturn in UK construction output

Construction output gains momentum amid strongest rise in new orders since April 2022

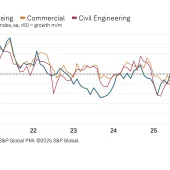

MAY PMI data signalled a modest upturn in overall UK construction output, driven by faster rises in commercial building and civil engineering activity. Meanwhile, house building remained by far the weakest-performing category of activity, with output declining at the steepest pace for three years.

Supply conditions continued to normalize in May, as highlighted by the greatest improvement in vendor lead times since August 2009. This helped to alleviate cost pressures across the construction sector, with the overall rate of input price inflation easing to its weakest for 32 months.

The headline seasonally adjusted S&P Global / CIPS UK Construction Purchasing Managers’ Index (PMI) – which measures month-on-month changes in total industry activity – registered 51.6 in May, up from 51.1 in April and above the neutral 50.0 mark for the fourth successive month. Although indicative of only modest growth, the latest reading pointed to the strongest upturn in total construction activity since February.

There were again divergent trends across the three main categories of construction activity. Commercial building (index at 54.2) was the best-performing segment, with output rising at a robust and accelerated pace. Construction companies cited a gradual turnaround in confidence among clients and faster decision-making on new projects. Civil engineering also gained momentum (index at 53.9), with growth hitting an 11-month high in May.

Worries about the impact of higher interest rates and subdued market conditions continued to dampen housing activity. Work on residential building projects decreased for the sixth month running and at the steepest pace since May 2020. Aside from the pandemic-related downturn, the latest reading for this category of construction activity (42.7) was the lowest for just over 14 years.

Meanwhile, total new business increased at a strong pace in May, despite weakness in the house building sector. The overall rise in construction order books was the strongest recorded since April 2022.

Supply conditions also improved considerably in May. Average lead times for the delivery of construction products and materials shortened to the greatest extent since August 2009. This was attributed to fewer logistics bottlenecks, alongside an improved balance between demand and supply.

Construction companies remain upbeat about their growth prospects for the year ahead, with around 45% of the survey panel expecting an increase in output levels, while only 14% predict a decline. That said, the degree of positive sentiment slipped to a four-month low in May. Survey respondents suggested that concerns about the UK economic outlook and the impact of rising interest rates were the main factors holding back growth projections in May.

Tim Moore, economics director at S&P Global Market Intelligence, who compile the survey, said: ‘May data highlighted a mixed picture across the UK construction sector as solid growth rates in commercial and civil engineering activity contrasted with a steeper downturn in house building. Rising demand among corporate clients and contract awards on infrastructure projects meanwhile underpinned the fastest rise in new orders since April 2022.

‘However, cutbacks to new residential building projects in response to rising interest rates and subdued housing market conditions resulted in the sharpest drop in housing activity for three years. This meant that residential work underperformed the rest of the construction sector by the greatest margin since October 2008. Survey respondents also commented on concerns about the broader UK economic outlook, which contributed to an overall drop in output growth projections to the lowest for four months.’