Ready-mixed concrete markets continue to be competitive

First published in the January 2017 issue of Quarry Management

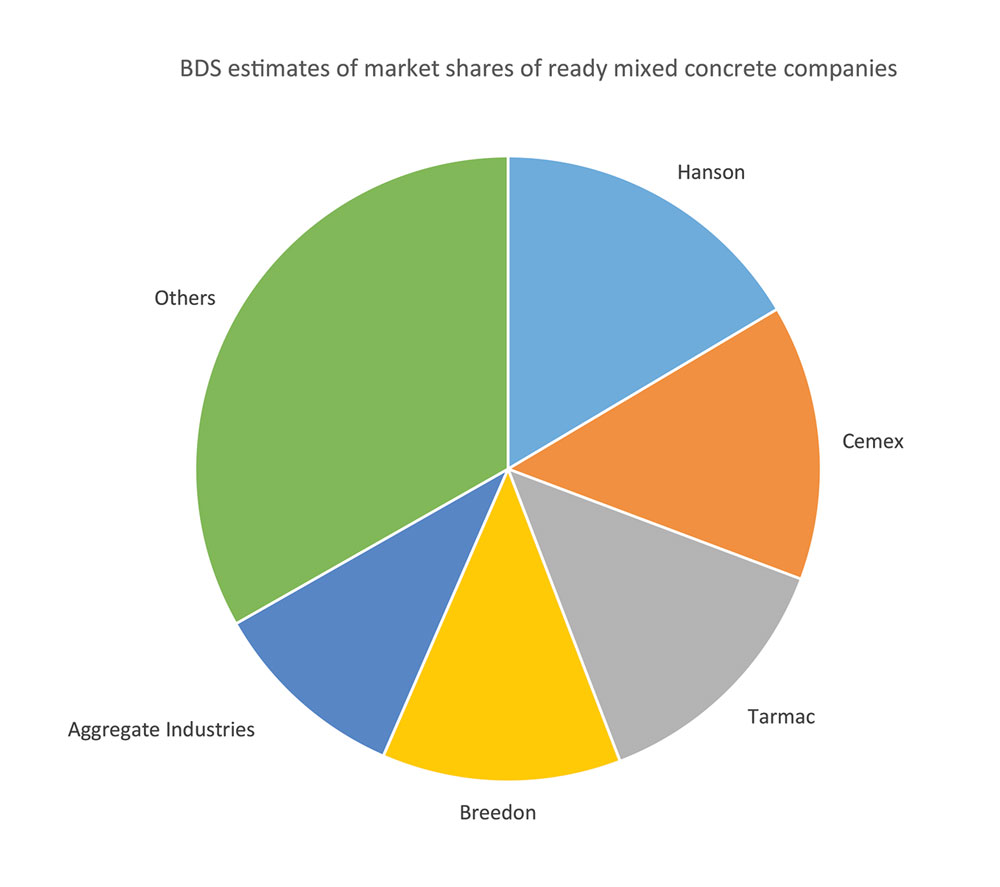

Although margins in ready-mixed concrete have improved in recent years, and are probably higher than they have been since 2008, the sector remains highly competitive. The top five companies – Hanson, CEMEX, Tarmac, Breedon and Aggregate Industries – represent around two thirds of the market. This is significant, but shares are lower than in related sectors such as aggregates and asphalt. In addition, there are around 400 other batch-mix and volumetric companies. In any typical town or city in the country, purchasers of ready-mixed concrete will have the choice of four or more suppliers to choose from.

Every year there are small but discernible changes in plant ownerships. Most new plants are established by independent companies. Volumetric concrete now represents 10% of the market and this is a sector where smaller companies dominate. A majority of plants that close are operated by a national business. Over a period of time, these trends can have a significant impact on the structure of the industry. For example, in 1989 the leading ready-mixed concrete company had more than 30% of the market. Despite no enforced disposals due to competition requirements, the share of this company has fallen to less than 20%. This has been the result of two major recessions and the growth of independent companies.

An analysis of historical events is interesting to understand how the industry arrived at its current situation, but it is an assessment of the likely future course of the industry that is key. Forecasts are sometimes proved wrong, but that should not stop commentators from making their best judgement. Only then can companies plan ahead.

Industry volumes are recovering from the worst of the recession. Current trends suggest that the market will continue to push ahead. The housing market is likely to enjoy increased activity. Volumes from some major projects, such as Crossrail, have tailed off, but Hinkley Point has finally been given the go-ahead. Much of the recovery was due to higher volumes in the South East. It is hoped that better market conditions will be enjoyed by suppliers throughout the country. BDS are forecasting a ready-mixed concrete market that will be around 10% higher by 2020 than it is now.

Within this overall market, what are the likely changes in industry structure?

Outside the top five companies, the next largest concrete supplier has a national share of 2%. The share of the next company is less than 1%. The opportunity for a major company acquiring a significant regional player has, therefore, all but disappeared. Typical future acquisitions will be of companies with less than five plants. It is likely that over the next decade, a handful of independent producers will emerge as regional players, with some ultimately acquired.

The growth of the volumetric sector has slowed, but further development can be expected. There is a trend of some volumetric companies entering the batch-mix sector, and vice versa. This will continue. One of the interesting things here is that the majors are always keen to ensure that their concrete plants can be supplied internally with aggregates. This is regarded as the correct strategy. Most independent concrete suppliers do not have their own source of aggregates, and yet they survive. A combination of low overheads and local knowledge and service ensures their survival.

Some of the major companies have recently entered the volumetric sector. It is unlikely that their involvement will remain at current levels. This is a sensible ‘test the water’ strategy. If successful, it would appear reasonable to expect the development of major companies in the volumetric sector. One other recent development has seen a major concrete supplier outsourcing its distribution to an external company. It will be interesting to see if competitors follow this path.

Another issue facing many companies is the age of existing concrete plants. Many will need replacing over the next five to 10 years. The ability to replace an ageing workforce is also a challenge. All these trends are analysed in the annual BDS report on ready-mixed concrete that assesses all companies in the industry.

This is the second of a series of features to be published every two months in Quarry Management by BDS Marketing Research into trends in the markets for aggregates, asphalt, concrete and cement. For further information on BDS-published reports on these markets and bespoke client research, please contact: andy.sales@bdsmarketing.co.uk; or tel: (01761) 433035.

- Subscribe to Quarry Management, the monthly journal for the mineral products industry, to read articles before they appear on Agg-Net.com